Send a message 0333 344 5890 |

- Home

- Knowledge

- Learning Hub

- Are Scope 3 emissions double counting?

Are Scope 3 emissions double counting?

To calculate the carbon footprint of any business, at Go Climate Positive, we provide a full implementation of the Green House Gas (GHG) protocolCorporate Accounting and Reporting Standard, which includes scope 3 emissions, or specifically the emissions from your value chain.

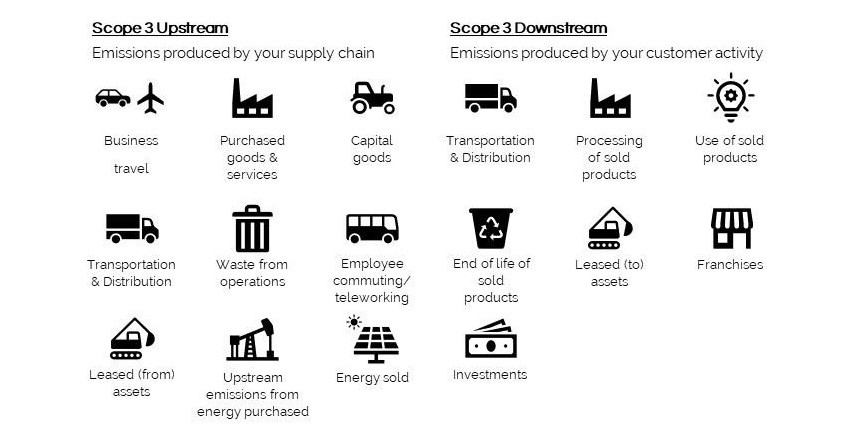

The scope 3 standard is internationally recognised and accounts for emissions within 15 categories that include activities both upstream and downstream of your business’s operations.

Included in these measurements are the emissions generated from activities in the creation, supply and distribution, through to the final disposal of the products or services a business sells.

Given the potential scale of these emissions, many organisations find that the largest part of their carbon footprint lands within Scope 3 and that these emissions fall outside of the organisations’ direct control. This makes them simultaneously the most important and the most challenging emissions to manage for many businesses.

Read more about Scope 1, 2 & 3 emissions here.

We select all the relevant categories to calculate the contribution made by your value chain to your overall carbon footprint.

Benefits of double counting value chain emissions

Using this method of data capture, double, triple or even quadruple counting is common across an economy of value chains under the present GHG Protocol. For example, when a steel manufacturer uses logistics companies to either transport raw materials or help dispose of the waste products from the production process, all organisations involved will be reporting emissions linked to the manufacture of that steel.

Given the nature of scope 3 emissions, understanding, and capturing their true value is more complex than comprehending scope 1 and 2 emissions, nevertheless, widening the scope for measurement and reporting on these sources provides significant opportunities for process improvement and carbon reduction but also ensures a reporting organisation has considered the wider impact of its activities and provides comprehensive evidence that a business takes its carbon reduction activities seriously.

There are also obvious environmental advantages for businesses that reduce their overall carbon footprint by accounting for scope 3 emissions. The more greenhouse gas (GHG) emissions that are accounted for and offset, the faster net zero goals can be achieved.

In summary, including scope 3 ‘value chain’ emissions in a business’s carbon footprint calculation is the only way that an organisation can measure its full impact on the climate. Using this method creates unavoidable double counting, as the scope 3 emissions are also captured in the carbon footprint of other organisations. But rather than be penalised for this increase in carbon emissions, under the greenhouse gas (GHG) protocols, organisations are celebrated as it demonstrates a real commitment to carbon reduction, while the more carbon that can be identified, reduced, or offset, the better for the environment.

If you would like help in identifying and mapping your scope 3 emissions, contact one of our carbon coaches for an in-depth discussion on carbon reduction.

Scope 3 and double counting

While the inclusion of these value chain emissions is good practice, at the start of a carbon footprint mapping process many businesses are concerned about the risk of “double counting”, specifically they fear that their results will be negatively affected – and carbon footprint increased – if emissions from other organisations are included within their measurements.

As with financial accounting, GHG accounting principles ensure the reported inventory represents a faithful, true and fair account of a company’s GHG emissions. However, when reviewing the value chain of any organisation, double counting between companies is an inherent characteristic of scope 3 emissions. Put simply, this is largely because what is considered as scope 3 emissions for one reporting organisation will also be classed as scope 1, 2 or 3 emissions for a supplier organisation and therefore included in the calculations for both the supplier and the reporting organisations.

Financial transactions work in the same way along the value chain as carbon transactions. When you buy a product the price you pay is a combination of the price that your supplier paid their supplier for the raw materials (their "scope 3 costs") plus the costs they added on in their operations (their "scope 1 and 2 costs"). So financial costs are double counted through the value chain in exactly the same way that carbon costs are. The only difference is that suppliers also typically add a profit margin to their financial transactions whereas carbon transactions are sold "at cost".

The road to net zero for any reporting business is a collaborative journey and so this double counting is largely advocated. The only consequence of this practice is that potentially two or more organisations take responsibility for the same emissions, and both strive to bring them down. This is a much less serious risk than the possibility of an organisation ignoring emissions it is solely responsible for.

If you would like some guidance on how to calculate your Scope 3 emissions get in touch with our Carbon Coaches today.

© Go Climate Positive Limited © Go Climate Positive Limited21 Naunton Lane, Cheltenham, Gloucs, UK GL53 7BJ |

|

|